Name

15分钟突破多周期协同策略基于风险收益比优化模型15-Minute-Breakout-Multi-Timeframe-Synergy-Strategy-with-Risk-Reward-Optimization-Model

Author

ianzeng123

Strategy Description

[trans]

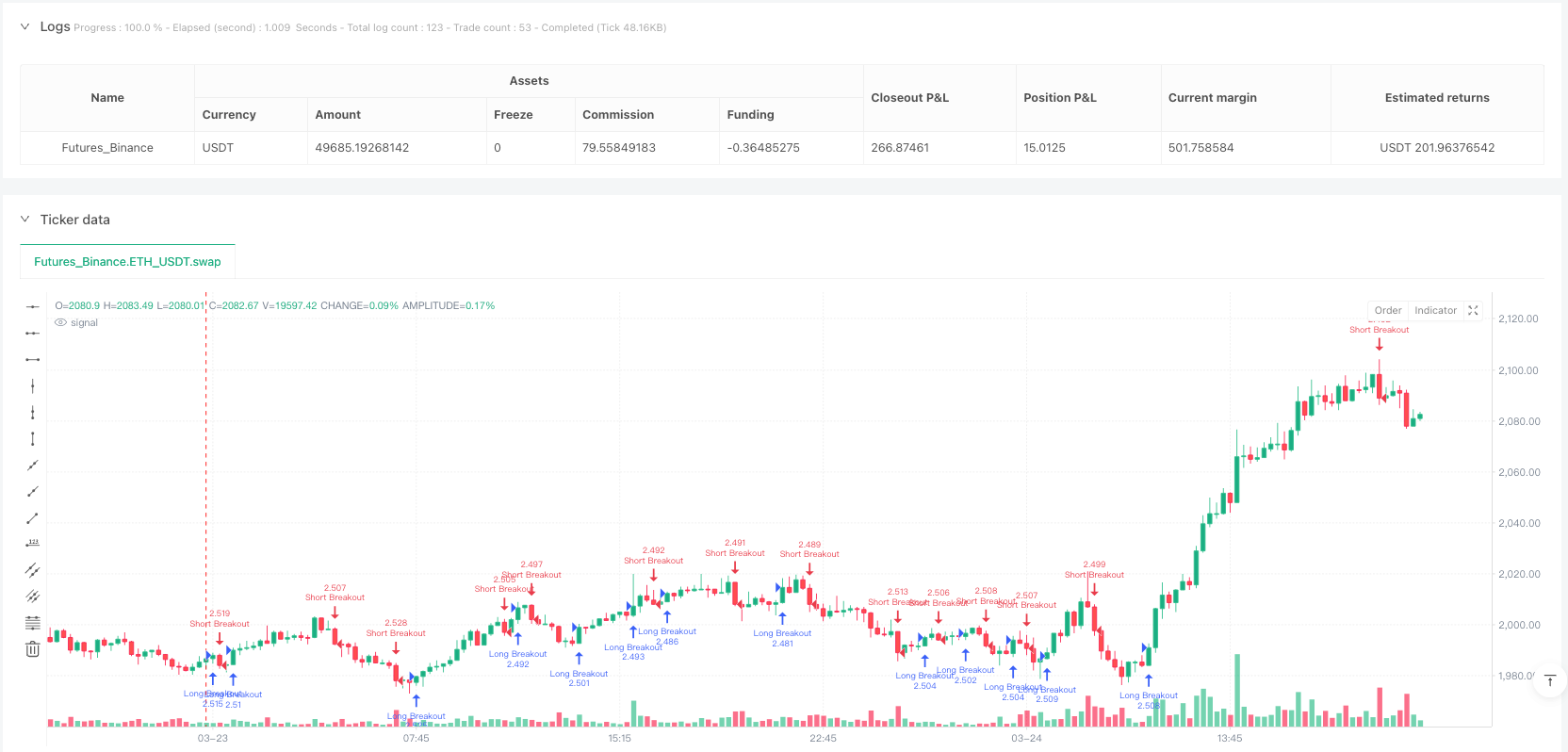

该策略是一个基于时间周期突破的量化交易系统,利用15分钟和2分钟两个时间周期的协同关系来确定交易信号。它通过观察2分钟K线的收盘价是否突破前一个完整15分钟K线的高点或低点来判断入场时机,同时设置了精确的风险控制机制,确保风险与收益比例为1:3,即每次风险单位可能获得3倍的盈利。策略本质上是捕捉短期价格突破后的动量延续,平均胜率约为30%,但由于良好的风险收益比设计,依然可以实现整体的正期望收益。

该策略的核心原理是通过多周期分析来识别价格突破信号。具体实现过程如下:

-

首先,策略使用

request.security函数获取15分钟周期的最高价、最低价和时间信息。 -

当检测到一个新的15分钟K线出现时(通过比较当前和前一个15分钟周期的时间),策略会保存前一个已完成15分钟K线的高点和低点作为突破参考点。

-

对于做多条件,策略判断当前2分钟K线的收盘价是否突破上一个完整15分钟K线的高点。满足条件时,入场价为2分钟K线收盘价,止损设置在上一个15分钟K线的低点,获利目标设定为入场价加上风险值的3倍(风险值=入场价-止损价)。

-

对于做空条件,策略判断当前2分钟K线的收盘价是否突破上一个完整15分钟K线的低点。满足条件时,入场价为2分钟K线收盘价,止损设置在上一个15分钟K线的高点,获利目标设定为入场价减去风险值的3倍(风险值=止损价-入场价)。

这种设计利用了突破交易的概念,同时结合了多周期分析的优势,使用较大时间周期(15分钟)来确定重要价格水平,而使用较小时间周期(2分钟)来优化入场时机,减少滑点并提高执行精度。

-

明确的风险管理: 策略设计了精确的风险收益比(1:3),确保每次交易的潜在收益是潜在损失的3倍,这使得即使胜率只有30%左右,仍然可以获得积极的期望收益。

-

多周期协同: 通过结合15分钟和2分钟两个时间周期,策略既能捕捉较大时间周期的重要价格水平,又能利用较小时间周期优化入场点,提高交易精确度。

-

自动化执行: 策略完全自动化,使用明确的入场和出场条件,减少了情绪干扰和主观判断。

-

资金管理集成: 策略采用账户权益百分比方式管理仓位(default_qty_value=10),确保风险与账户规模成比例增长或下降。

-

适应性强: 代码结构简洁清晰,易于扩展和修改,可以应用于不同市场和产品。

-

低胜率风险: 策略平均胜率约为30%,这意味着大多数交易会导致小额亏损。对于一些交易者来说,连续的亏损交易可能导致心理压力和过早放弃策略。

-

突破假信号: 价格突破后可能不会持续朝预期方向移动,导致频繁止损触发。特别是在横盘整理或高波动市场中,假突破现象更为普遍。

-

滑点风险: 在市场快速移动时,实际执行价格可能与策略计划价格存在差异,影响风险收益比的精确实现。

-

过度交易风险: 由于策略基于短周期(2分钟)执行交易,可能导致过度交易,增加交易成本。

-

市场环境依赖: 该策略在趋势明显的市场中表现较好,而在区间震荡市场中可能效果不佳。

解决方法:

- 添加额外的过滤条件,如趋势指标或波动率指标,减少假信号。

- 考虑设置每日最大交易次数限制,避免过度交易。

- 在低波动或高波动时期调整风险参数或暂停策略。

- 定期回测和优化策略参数,确保适应当前市场环境。

-

添加趋势过滤器: 在执行突破交易前,引入趋势确认指标(如移动平均线、MACD等),仅在与大趋势一致时入场,可以显著提高策略胜率。

-

动态风险收益比: 目前策略使用固定的1:3风险收益比,可以考虑根据市场波动性动态调整,例如在波动性高的市场中采用更保守的目标。

-

时间过滤: 添加时间过滤条件,避免在市场开盘、收盘或波动性特别低的时段交易。

-

部分止盈机制: 实现分段获利功能,在价格达到一定目标时平掉部分仓位,让剩余仓位继续追踪趋势,提高整体盈利能力。

-

自适应参数: 将固定参数(如15分钟周期)改为基于市场条件自动调整的动态参数,使策略能更好适应不同市场环境。

-

交易量确认: 加入成交量分析,确保价格突破伴随足够的交易量,这通常能提高突破信号的可靠性。

这些优化方向主要针对提高策略的胜率和稳定性,同时保持其核心优势——明确的风险管理和多周期协同特性。通过引入更多市场因素的考量,可以减少假信号,提高每笔交易的成功概率。

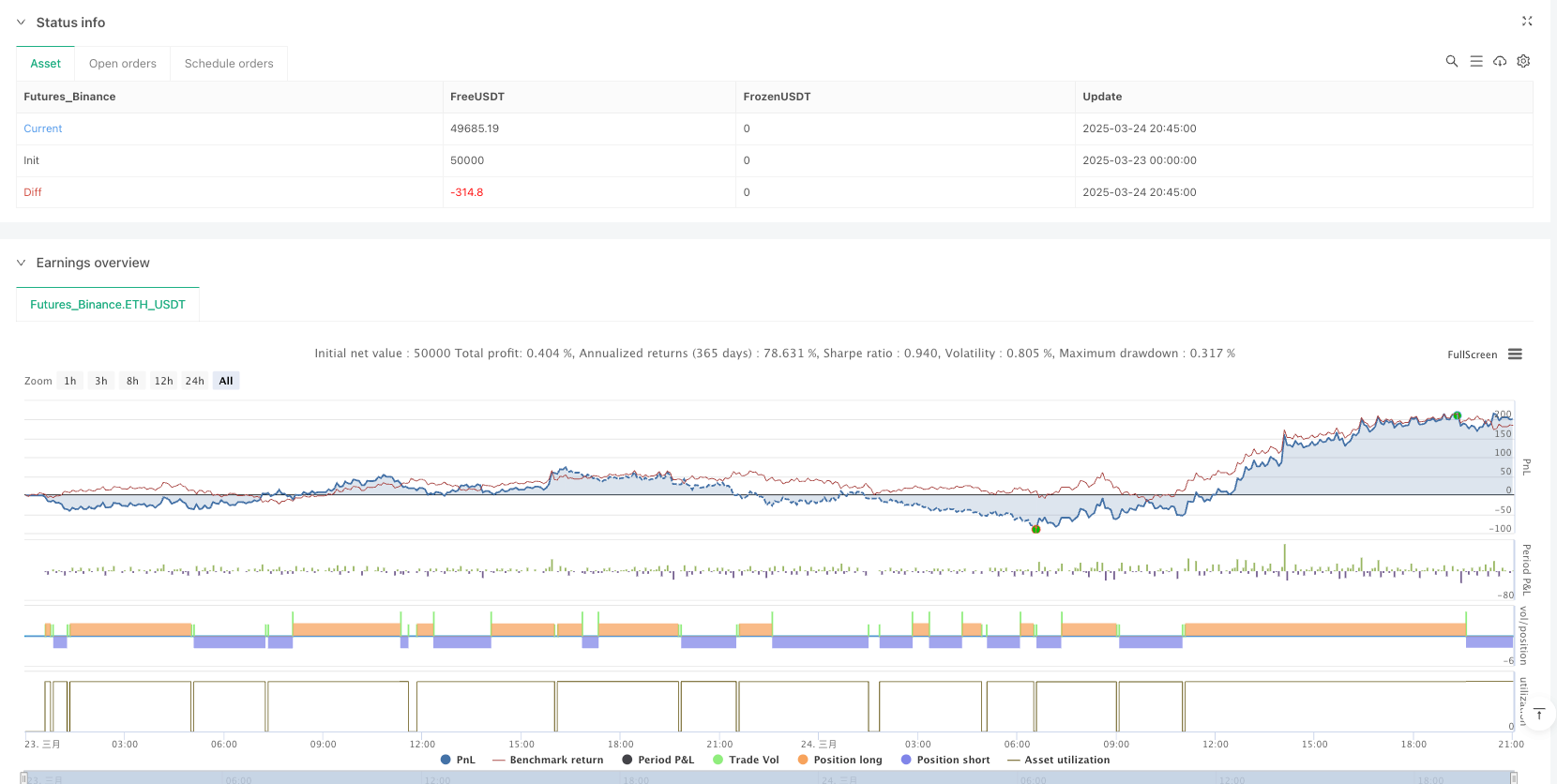

"15分钟突破多周期协同策略基于风险收益比优化模型"是一个结构清晰、逻辑严谨的量化交易系统,它通过结合不同时间周期的价格信息,捕捉突破后的动量机会。尽管策略胜率不高(约30%),但通过精心设计的1:3风险收益比机制,实现了正的期望收益。

策略的核心优势在于其严格的风险控制、明确的入场出场规则和多周期协同分析方法。主要风险来自于假突破信号和低胜率带来的心理压力。未来优化方向应着重于提高信号质量,减少假突破交易,并考虑添加趋势过滤和动态参数调整功能。

对于追求中短期交易机会的量化交易者来说,这是一个值得考虑的基础策略框架,可以根据个人风险偏好和交易目标进行进一步定制和优化。 ||

This strategy is a quantitative trading system based on timeframe breakout, utilizing the synergistic relationship between 15-minute and 2-minute timeframes to determine trading signals. It identifies entry opportunities by observing whether the 2-minute candle's closing price breaks through the high or low of the previous completed 15-minute candle, while implementing a precise risk control mechanism that ensures a risk-to-reward ratio of 1:3, meaning each unit of risk can potentially yield 3 units of profit. The strategy essentially captures momentum continuation after short-term price breakouts, with an average win rate of approximately 30%, but can still achieve an overall positive expected return due to its well-designed risk-reward ratio.

The core principle of this strategy is to identify price breakout signals through multi-timeframe analysis. The specific implementation process is as follows:

-

First, the strategy uses the

request.securityfunction to obtain the highest price, lowest price, and time information for the 15-minute timeframe. -

When a new 15-minute candle is detected (by comparing the current and previous 15-minute period times), the strategy saves the high and low points of the previous completed 15-minute candle as breakout reference points.

-

For long conditions, the strategy determines whether the current 2-minute candle's closing price breaks through the high of the last complete 15-minute candle. When this condition is met, the entry price is the 2-minute candle's closing price, the stop loss is set at the low of the previous 15-minute candle, and the profit target is set at the entry price plus 3 times the risk value (risk value = entry price - stop loss price).

-

For short conditions, the strategy determines whether the current 2-minute candle's closing price breaks through the low of the last complete 15-minute candle. When this condition is met, the entry price is the 2-minute candle's closing price, the stop loss is set at the high of the previous 15-minute candle, and the profit target is set at the entry price minus 3 times the risk value (risk value = stop loss price - entry price).

This design leverages the concept of breakout trading while combining the advantages of multi-timeframe analysis, using a larger timeframe (15 minutes) to determine important price levels and a smaller timeframe (2 minutes) to optimize entry timing, reduce slippage, and improve execution precision.

-

Clear Risk Management: The strategy features a precise risk-reward ratio (1:3), ensuring that the potential return for each trade is three times the potential loss, which allows for positive expected returns even with a win rate of only around 30%.

-

Multi-Timeframe Synergy: By combining 15-minute and 2-minute timeframes, the strategy can both capture important price levels from the larger timeframe and optimize entry points using the smaller timeframe, improving trading precision.

-

Automated Execution: The strategy is fully automated with clear entry and exit conditions, reducing emotional interference and subjective judgment.

-

Integrated Capital Management: The strategy adopts a percentage of equity approach for position sizing (default_qty_value=10), ensuring that risk scales proportionally with account size.

-

High Adaptability: The code structure is concise and clear, making it easy to extend and modify for application across different markets and products.

-

Low Win Rate Risk: The strategy has an average win rate of approximately 30%, meaning most trades will result in small losses. For some traders, consecutive losing trades may cause psychological pressure and premature abandonment of the strategy.

-

False Breakout Signals: After a price breakout, the price may not continue to move in the expected direction, leading to frequent stop-loss triggers. This is especially common in ranging markets or highly volatile conditions.

-

Slippage Risk: During rapid market movements, the actual execution price may differ from the planned price, affecting the precise implementation of the risk-reward ratio.

-

Overtrading Risk: Since the strategy executes trades based on a short timeframe (2 minutes), it may lead to overtrading and increased transaction costs.

-

Market Environment Dependency: This strategy performs better in trending markets and may underperform in range-bound, oscillating markets.

Solutions:

- Add additional filtering conditions, such as trend indicators or volatility indicators, to reduce false signals.

- Consider setting daily maximum trade limits to avoid overtrading.

- Adjust risk parameters or pause the strategy during periods of low or high volatility.

- Regularly backtest and optimize strategy parameters to ensure adaptation to the current market environment.

-

Add Trend Filters: Introduce trend confirmation indicators (such as moving averages, MACD, etc.) before executing breakout trades, only entering when aligned with the larger trend, which can significantly improve the strategy's win rate.

-

Dynamic Risk-Reward Ratio: The strategy currently uses a fixed 1:3 risk-reward ratio, but could be enhanced by dynamically adjusting this ratio based on market volatility, such as adopting more conservative targets in highly volatile markets.

-

Time Filtering: Add time-based filtering conditions to avoid trading during market open, close, or particularly low volatility periods.

-

Partial Profit-Taking Mechanism: Implement a staged profit-taking functionality that closes part of the position when certain price targets are reached, allowing the remaining position to continue tracking the trend, improving overall profitability.

-

Adaptive Parameters: Transform fixed parameters (such as the 15-minute period) into dynamic parameters that automatically adjust based on market conditions, enabling the strategy to better adapt to different market environments.

-

Volume Confirmation: Incorporate volume analysis to ensure price breakouts are accompanied by sufficient trading volume, which typically enhances the reliability of breakout signals.

These optimization directions primarily aim to improve the strategy's win rate and stability while maintaining its core advantages—clear risk management and multi-timeframe synergy. By introducing consideration of more market factors, false signals can be reduced, increasing the probability of success for each trade.

The "15-Minute Breakout Multi-Timeframe Synergy Strategy with Risk-Reward Optimization Model" is a clearly structured, logically rigorous quantitative trading system that captures momentum opportunities after breakouts by combining price information from different timeframes. Despite the strategy's relatively low win rate (approximately 30%), it achieves positive expected returns through a carefully designed 1:3 risk-reward ratio mechanism.

The strategy's core strengths lie in its strict risk control, clear entry and exit rules, and multi-timeframe synergistic analysis method. The main risks come from false breakout signals and the psychological pressure associated with a low win rate. Future optimization should focus on improving signal quality, reducing false breakout trades, and considering the addition of trend filtering and dynamic parameter adjustment capabilities.

For quantitative traders seeking medium to short-term trading opportunities, this represents a worthwhile basic strategy framework that can be further customized and optimized according to individual risk preferences and trading objectives.[/trans]

Source (PineScript)

/*backtest

start: 2025-03-23 00:00:00

end: 2025-03-24 21:00:00

period: 15m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("15-min Breakout via 2-min Candle (R:R=1:3)",

overlay=true,

initial_capital=100000,

default_qty_type=strategy.percent_of_equity,

default_qty_value=10)

//-----------------------------------------------------

// 1) Retrieve 15-min high/low & time via request.security

//-----------------------------------------------------

fifteenHigh = request.security(syminfo.tickerid, "15", high)

fifteenLow = request.security(syminfo.tickerid, "15", low)

time15 = request.security(syminfo.tickerid, "15", time)

//-----------------------------------------------------

// 2) Store the most recent closed 15-min bar's high/low

//-----------------------------------------------------

// We use a var variable (stored over time) and update it

// whenever a NEW 15-min bar is detected.

var float last15High = na

var float last15Low = na

// A new 15-min bar (in the "15" series) is indicated when time15 changes.

bool new15bar = time15 != time15[1]

// Update high/low when a new 15-min bar starts

if new15bar

// [1] = previous closed 15-min bar value

last15High := fifteenHigh[1]

last15Low := fifteenLow[1]

//-----------------------------------------------------

// 3) Long position: 2-min close > most recent closed 15-min high

//-----------------------------------------------------

bool longCondition = not na(last15High) and close > last15High

if longCondition

// Entry is 2-min close

float stopPrice = last15Low

float risk = close - stopPrice

float takeProfit = close + 3 * risk

strategy.entry("Long Breakout", strategy.long)

strategy.exit("Long Exit (SL/TP)", "Long Breakout", stop=stopPrice, limit=takeProfit)

//-----------------------------------------------------

// 4) Short position: 2-min close < most recent closed 15-min low

//-----------------------------------------------------

bool shortCondition = not na(last15Low) and close < last15Low

if shortCondition

float stopPrice = last15High

float risk = stopPrice - close

float takeProfit = close - 3 * risk

strategy.entry("Short Breakout", strategy.short)

strategy.exit("Short Exit (SL/TP)", "Short Breakout", stop=stopPrice, limit=takeProfit)

Detail

https://www.fmz.com/strategy/488850

Last Modified

2025-03-31 17:32:58